All Categories

Featured

[/image][=video]

[/video]

Holding cash in an IUL repaired account being credited passion can frequently be better than holding the money on deposit at a bank.: You've constantly desired for opening your own bakery. You can obtain from your IUL plan to cover the initial expenses of leasing a space, purchasing tools, and working with team.

Credit score cards can give a flexible method to borrow money for really temporary durations. Borrowing money on a credit scores card is usually extremely pricey with annual percent prices of passion (APR) frequently reaching 20% to 30% or even more a year.

The tax therapy of plan finances can vary significantly depending on your nation of residence and the details regards to your IUL policy. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, plan lendings are generally tax-free, supplying a substantial advantage. In other territories, there might be tax obligation effects to consider, such as prospective taxes on the loan.

Term life insurance coverage only provides a death benefit, with no cash money worth accumulation. This indicates there's no cash money value to obtain versus. This write-up is authored by Carlton Crabbe, Chief Exec Police Officer of Funding for Life, a professional in providing indexed universal life insurance policy accounts. The details provided in this write-up is for educational and educational objectives only and must not be understood as economic or investment suggestions.

How Do I Start My Own Bank?

Think of stepping into the monetary universe where you're the master of your domain, crafting your own path with the skill of a skilled lender but without the restraints of imposing organizations. Invite to the world of Infinite Financial, where your monetary destiny is not just a possibility but a substantial reality.

Uncategorized Feb 25, 2025 Money is one of those things we all manage, yet most of us were never actually taught just how to utilize it to our advantage. We're informed to save, spend, and budget, yet the system we run in is created to maintain us dependent on banks, continuously paying rate of interest and charges just to access our own cash.

She's a professional in Infinite Banking, a method that assists you take back control of your funds and build real, lasting riches. And depend on methis isn't some "financing bro" magic method. It's a genuine strategy that well-off households like the Rockefellers and Rothschilds have actually been making use of for generations. Let's get involved in it.

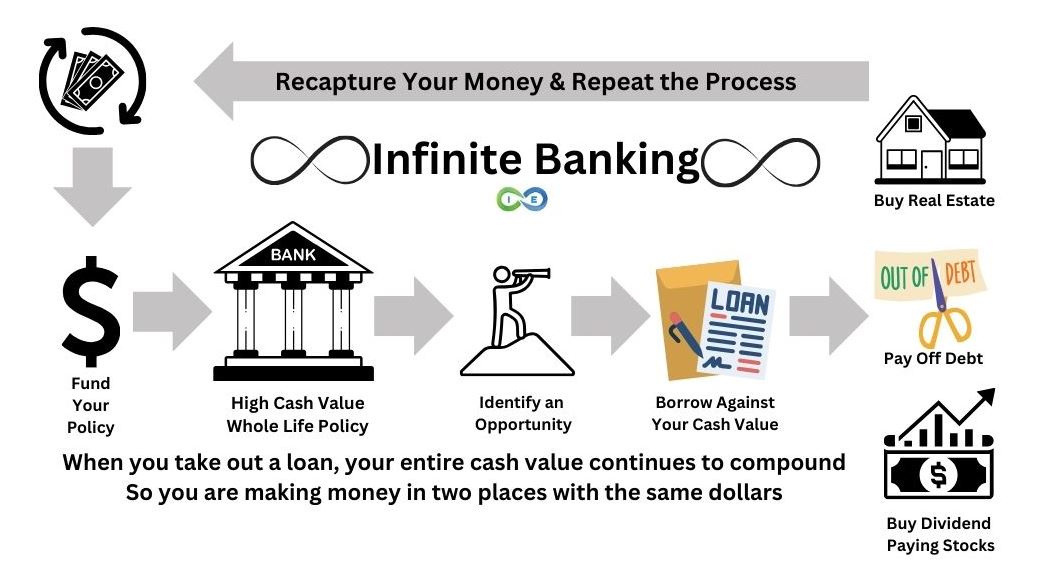

Now, prior to you roll your eyes and assume, Wait, life insurance? That's boring.stay with me. This isn't the sort of life insurance policy the majority of people have. This is a high-cash-value policy that allows you to: Shop your money in an area where it expands tax-free Borrow versus it whenever you need to make investments or significant purchases Earn undisturbed substance interest on your cash, also when you borrow versus it Consider exactly how a bank functions.

With Infinite Financial, you end up being the bank, making that interest instead of paying it. It's a total paradigm change, and as soon as you see exactly how it functions, you can't unsee it. For the majority of us, cash flows out of our hands the 2nd we get it. We pay costs, make purchases, pay for debtour dollars are frequently leaving us.

Life Insurance Banking

The insurance coverage business does not require to get "repaid," since it will simply be deducted from what gets distributed to your beneficiaries upon your expiration day, as Hannah so euphemistically called it. You pay on your own back with interest, similar to a bank wouldbut now, you're the one benefiting. Let that sink in.

It's about redirecting your cash in such a way that constructs riches as opposed to draining it. If you're in genuine estateor wish to bethis approach is a found diamond. Let's say you wish to acquire a financial investment residential or commercial property. Rather than going to a financial institution for a funding, you obtain from your own policy for the down payment.

You utilize the loan to buy your building. Rental income or benefit from the bargain pay back your plan rather than a financial institution. This implies you're constructing equity in your plan AND in actual estate at the exact same time. That's what Hannah calls double-dippingand it's specifically how the rich maintain growing their cash.

Infinite Concept

Allow's remove a couple of up. Here's the thingthis isn't an investment; it's a financial savings strategy. Investments involve risk; this doesn't. Your money is guaranteed to expand no matter what the supply market is doing. Maybe, however this isn't about either-or. You can still buy real estate, stocks, or businessesbut you run your money via your policy first, so it keeps growing while you invest.

Make certain you collaborate with an Infinite Financial Principle (IBC) practitioner who recognizes how to establish it up appropriately. This method is a total frame of mind change. We have actually been trained to think that banks hold the power, but the truth isyou can take that power back. Hannah's household has been using this technique given that 2008, and they currently have more than 38 policies funding realty, investments, and their family's economic heritage.

Becoming Your Own Lender is a message for a ten-hour program of guideline regarding the power of dividend-paying entire life insurance policy. It is not a sales device forever insurance coverage representatives. It is education that the life insurance policy sector should have taught during the last 200 years. The sector has concentrated on the fatality benefit high qualities of the contract and has actually neglected to adequately explain the funding capabilities that it presents for the plan owners.

This publication shows that your demand for finance, during your lifetime, is much above your requirement for protection. Solve for this need with this instrument and you will certainly wind up with even more life insurance policy than the business will certainly release on you. A lot of every person knows with the reality that a person can borrow from an entire life plan, yet because of just how little costs they pay, there is minimal access to cash to finance major items needed throughout a lifetime.

Really, all this book contributes to the equation is range.

{kind=link}

Latest Posts

Infinite Banking Reviews

Becoming Your Own Banker And Farming Without The Bank

Want To Build Tax-free Wealth And Become Your Own ...